![]()

Python and the Financial Community¶

A Subjective and Biased Overview

The Python Language¶

Black-Scholes-Merton (1973) SDE of geometric Brownian motion.

$$ dS_t = rS_tdt + \sigma S_t dZ_t $$

Monte Carlo simulation: draw $I$ standard normally distributed random number $z_t^i$ and apply them to the following by Euler disctretization scheme to simulate $I$ end values of the GBM:

$$ S_{T} = S_0 \exp \left(\left( r - \frac{1}{2} \sigma^2\right) T + \sigma \sqrt{T} z_T \right) $$

Latex description of Euler discretization.

S_T = S_0 \exp (( r - 0.5 \sigma^2 ) T + \sigma \sqrt{T} z_T)

Python implementation of algorithm.

from pylab import *

S0 = 100.; r = 0.01; T = 0.5; sigma = 0.2

ST = S0 * exp((r - 0.5 * sigma ** 2) * T

+ sigma * sqrt(T) * standard_normal(10000))

Interactive visualization of simulation results.

%matplotlib inline

hist(ST, bins=40);

grid(True)

The Python Ecosystem¶

- IPython (Notebook)

- NumPy (fast, vectorized array operations)

- SciPy (collection of scientific classes/functions)

- pandas (times series and tabular data)

- PyTables (hardware-bound IO operations)

- scikit-learn (machine learning algorithms)

- statsmodels (statistical classes/functions)

- xlwings (Python-Excel integration)

Financial Libraries¶

By others:

- zipline (backtesting of trading algos)

- matplotlib.finance (financial plots)

- Python wrappers (QuantLib)

By us:

- DEXISION – GUI-based financial engineering

- DX Analytics – global valuation of multi-risk derivatives and portfolios

APIs¶

- OANDA (fx trading platform)

- Thomson Reuters (wrapper for unified API in the making)

- ...

Integration¶

- C/C++ (natively)

- Julia (IPython)

- JavaScript (IPython)

- R (IPython/rpy2)

- Matlab (NumPy)

- ...

Pushing data from Python to R.

%load_ext rpy2.ipython

X = arange(100)

Y = 2 * X + 5 + 2 * standard_normal(len(X))

%Rpush X Y

Generating plots with R.

%R plot(X, Y, pch=19, col='blue'); grid(); title("R Plot with IPython")

Doing statistics in R.

%R print(summary(lm(Y~X)))

Pulling data from R to Python.

%R c = coef(lm(Y~X))

%Rpull c

c

Performance¶

Finance algorithms are loop-heavy; Python loops are slow; Python is too slow for finance.

def counting_py(N):

s = 0

for i in xrange(N):

for j in xrange(N):

s += int(cos(log(1)))

return s

N = 2000

%time counting_py(N)

# memory efficient but slow

First approach: vectorization with NumPy.

%%time

arr = ones((N, N))

print int(sum(cos(log(arr))))

# much faster but NOT memory efficient

arr.nbytes

Second approach: dynamic compiling with Numba.

import numba

counting_nb = numba.jit(counting_py)

%time counting_nb(N)

%timeit counting_nb(N)

# even faster AND memory efficient

Hardware-bound IO operations are standard for Python.

arr = standard_normal((12500, 10000))

arr.nbytes

# a giga byte worth of data

%time save('data', arr)

!ls -n data*

!rm data*

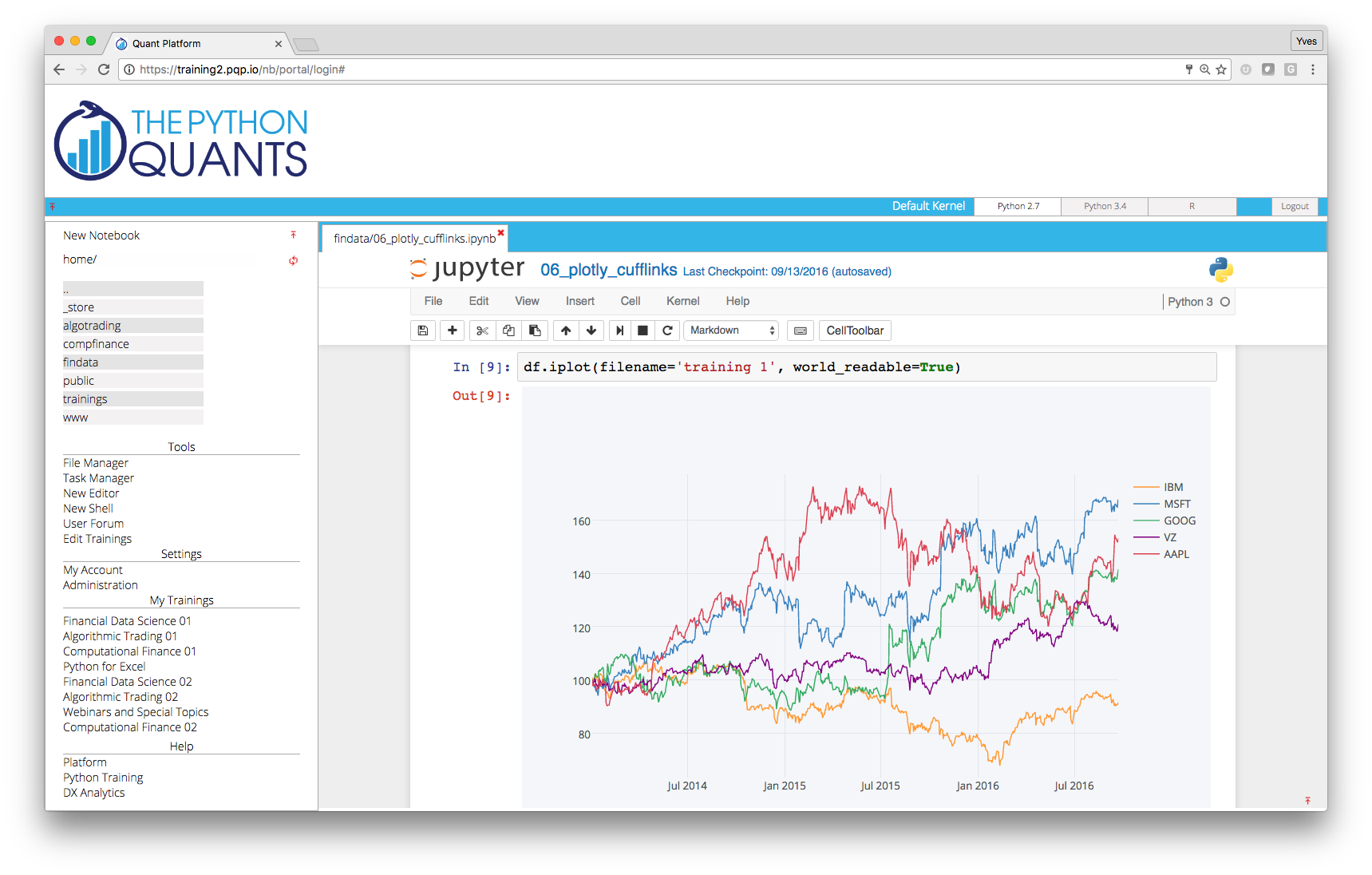

Python Quant Platform¶

Integrating it all and adding collaboration and scalability (http://quant-platform.com).

The Large Banks¶

- Bank of America Merill Lynch (Quartz platform)

- JPMorgan Chase (Athena platform)

- ...

The Hedge Funds¶

- AQR Capital Management (origin of pandas)

- Two Sigma Investments (large scale data analytics)

- ARC Investments (full-fledged Python for vol trading)

- ...

Innovators in the Space¶

- Quantopian (algo trading & backtesting)

- Washington Square Technologies (trade & risk platform)

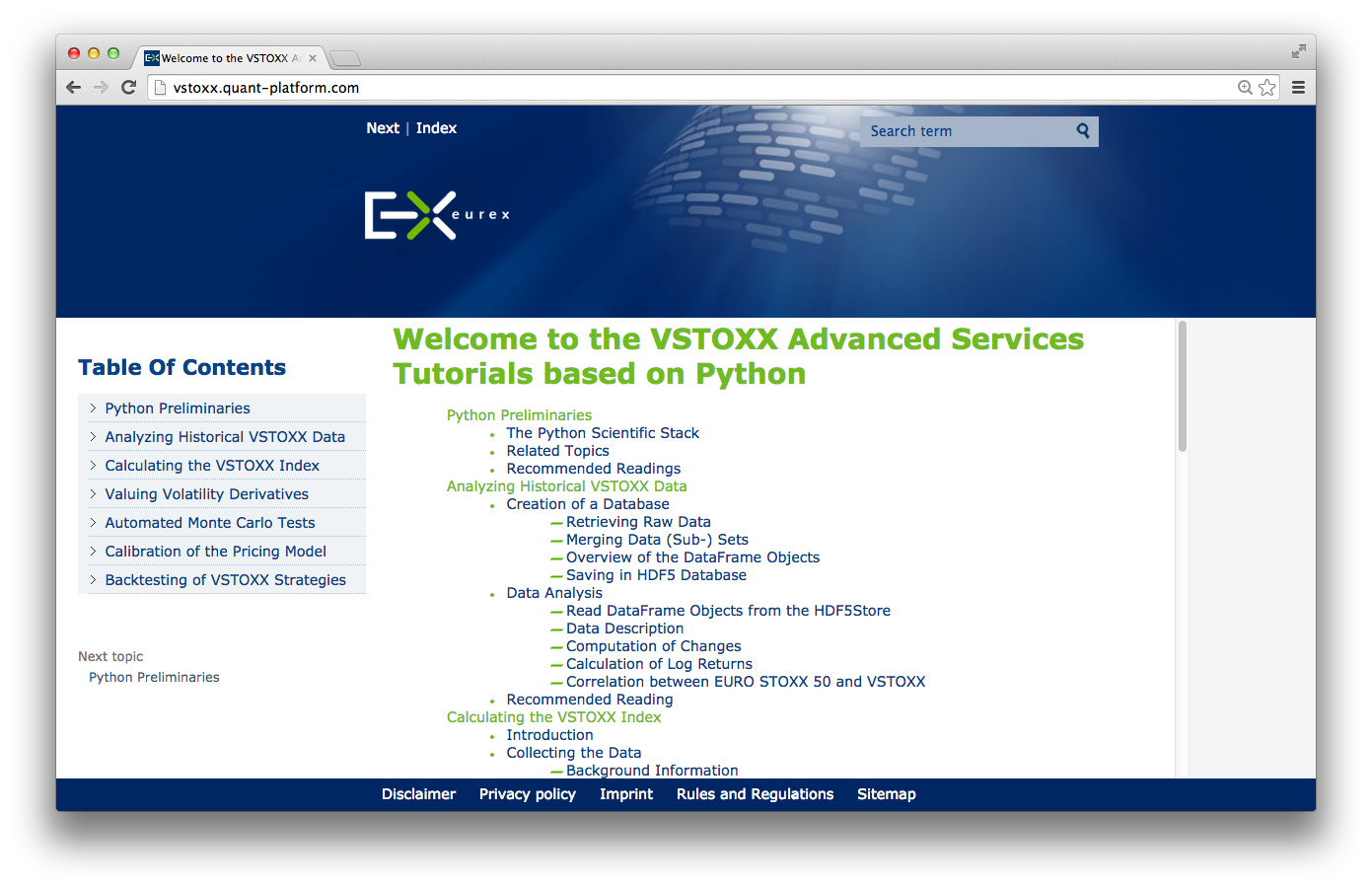

- Deutsche Boerse/Eurex (VSTOXX and Variance Advanced Services)

- ...

Python-based tutorials by Eurex (http://www.eurexchange.com/vstoxx/).

Books¶

By others:

- Python for Financial Modelling @ Wiley Finance (2009)

- Python for Finance @ Packt Publishing (2014)

By myself:

- Python for Finance – Analyze Big Financial Data @ O'Reilly (2014)

- Derivatives Analytics with Python @ Wiley Finance (2015)

Integrated offering: book + notebooks + platform + training + ...

Financial Research¶

"The appendices present an implementation in Python of our experiments." (p. 3)

Education¶

- Master of Financial Engineering @ Baruch College CUNY

- Master of Data Science @ City University of New York

- Numerical Option Pricing with Python @ Saarland University

- ...

"Knowledge and Skills: Our graduates have working experience with C++, VBA, Python, R, and Matlab for financial applications. They share an exceptionally strong work ethic and possess excellent interpersonal, teamwork, and communication skills."

Training¶

By others:

- Python for Finance @ Continuum Analytics

- Python for Finance @ Enthought

By myself:

- Python for Quant Finance @ Python for Quant Finance Meetup Group

- Python for Finance @ http://quantshub.com

- NumPy & pandas for Finance @ CQF Institute/Fitch Learnings

- ...

Meetups¶

For Python Quants Conference¶

- 1st conference in New York City on 14. March 2014

- 2nd conference in London on 28. November 2014

- 3rd conference planned for QI 2015 in Asia (eg Shanghai)

Contact us¶

Please contact us if you have any questions or want to get involved in our Python community events.

![]()

Python Quant Platform | http://quant-platform.com

Derivatives Analytics with Python | Derivatives Analytics @ Wiley Finance

Python for Finance | Python for Finance @ O'Reilly